Highlights

- The last and most recent USD 500 movement for gold prices has been the quickest to happen, in just 7.5 months amid global uncertainties (2023-24).

- The precious metal has proved almost a perfect hedge to equity markets during times of crisis.

- This year, we have already seen global central banks adding 473 metric tonnes in the first six months.

- Growing expectations of an interest rate cut by the US Federal Reserve have also driven up the recent price movement.

Gold price in the international market recently hit an all-time high of USD 2,500 per ounce on August 16, 2024. We've compiled some interesting data points about this precious metal's journey:

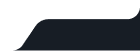

Price Journey So Far

- Looking at historical gold price movements this century:It took ~4 years for gold to move from USD 500 to USD 1,000 per ounce (2005-09).

- The next USD 500 price movement came quickly in 1.7 years during the global financial crisis (2009-11).

- Prices then stabilized, taking around 12.5 years for gold to move to the next USD 500 increment (2011-23).

- The last USD 500 movement has been the fastest, happening in just 7.5 months amid global uncertainties (2023-24).

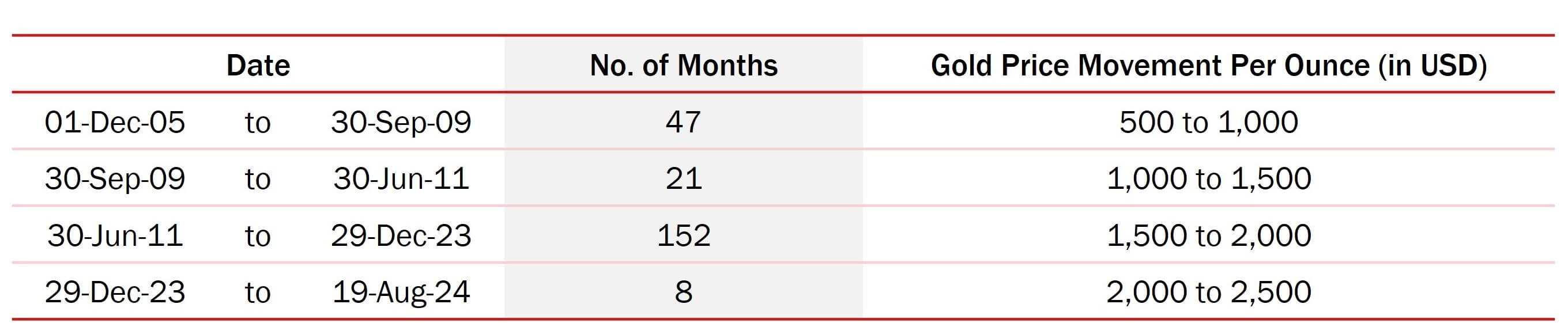

Hedge to Equity?

The precious metal has proved to be a near-perfect hedge to equity markets during times of crisis. Below are some down-market scenarios where gold has generated positive returns.

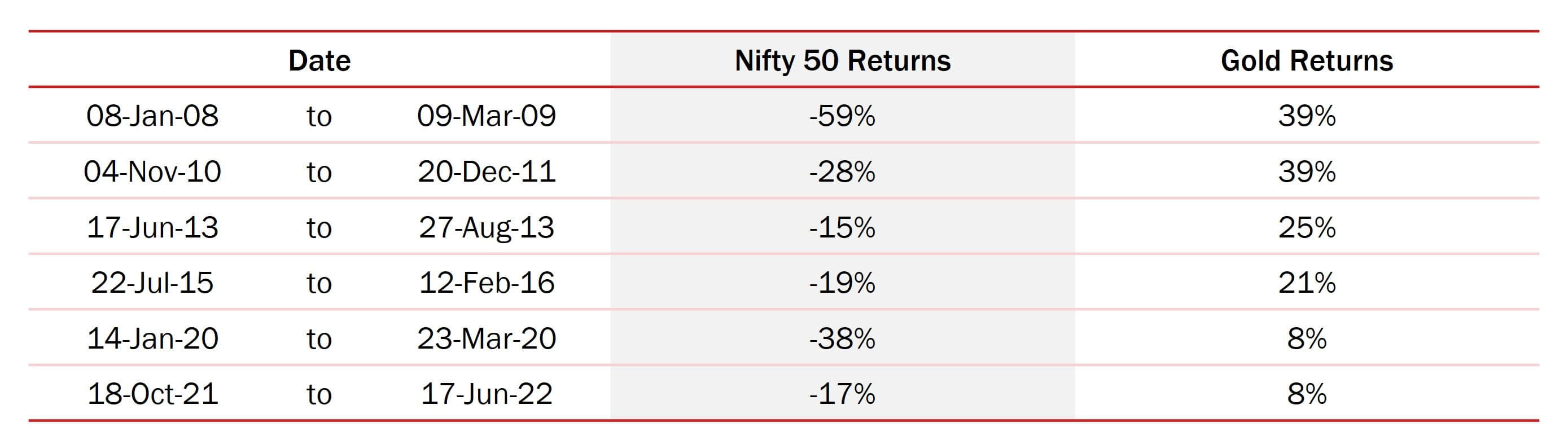

Central Banks

Central banks have consistently added gold to their vaults. This year alone, they have accumulated 473 metric tonnes in the first six months, aligning with the previous two-year purchases of ~1,000 metric tonnes/year.

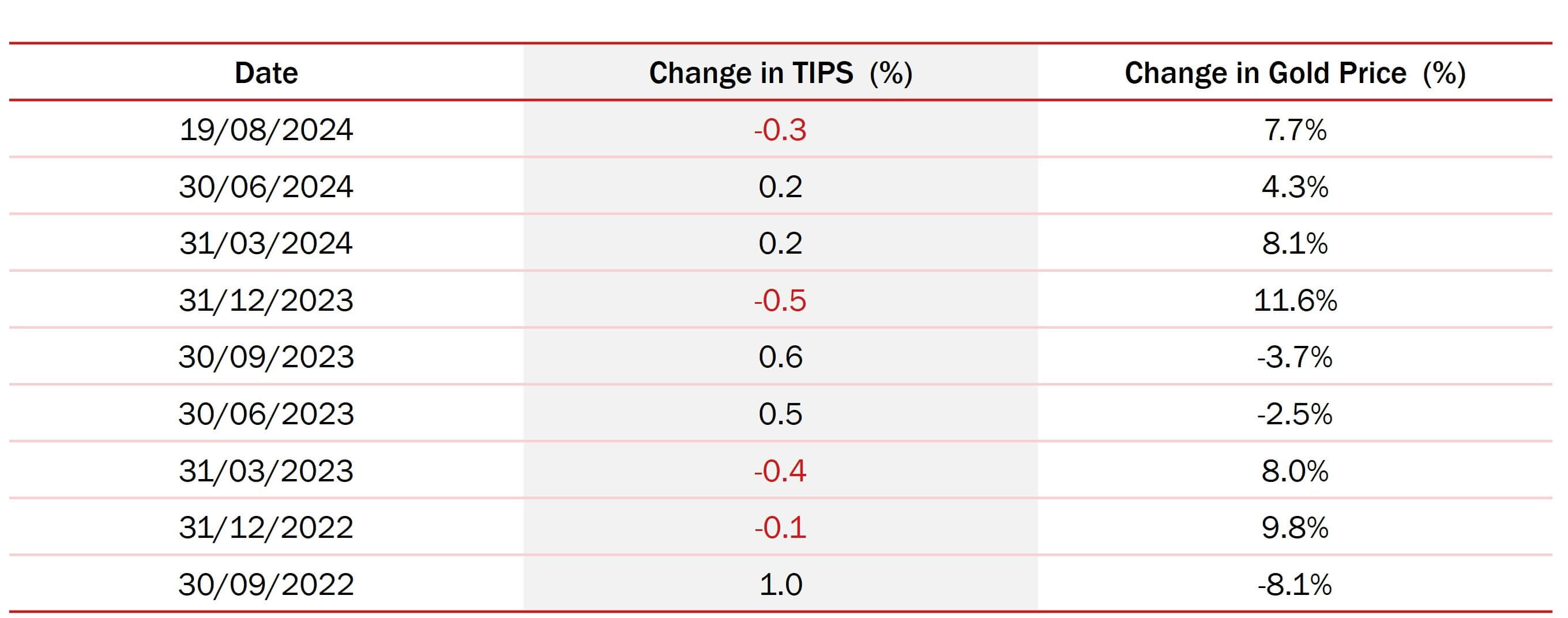

TIPS 10Y and Gold Price

The negative correlation between TIPS 10Y and gold price has held true this quarter. During this period, gold prices rose 7.7%, while US 10-year TIPS declined by 32 bps from 2.11% to 1.79%.

Reasons for the Current Rally in Gold Prices

- Continued aggressive buying by global central banks, maintaining a run rate of ~1,000 metric tonnes/year since 2022 compared to ~500 metric tonnes/year from 2012 to 2021.

- Ongoing geopolitical tensions, including the Israel-Hamas conflict and Russia-Ukraine war, driving demand for safe-haven assets.

- Growing expectations of an interest rate cut by the US Federal Reserve, pushing prices higher.

Conclusion

From a medium to long term perspective, we continue to remain positive on gold due to weakness in the dollar, expectation of rate cuts, increase in central bank buying and geo-political risks. Disciplined portfolios following asset allocation should have some allocation to gold as it has low correlation to the equity asset class (which gets further lower or negative in times of enhanced risks) and thereby provides a good hedge.

For important details, please read our disclaimer.

Updates

Subscribe to our latest news, insights, opinions and more

Hi there!

Tell us a little about yourself and your communication preferences.